Until recently I hadn’t considered the true cost of owning, maintaining, insuring and fuelling my car, and whether or not it represented good value for the amount of use I got from it. Then I heard about monthly vehicle subscriptions. So, what are they and will they save me any money? And in a COVID world, where people are nervous about buying large, new assets like cars, are they the solution?

The traditional narrative on car ownership has changed massively over the last decade. For a long time now owning a car in cities like London, Singapore or New York simply didn’t make sense given the reliability and affordability of public transport. With the rise of ride-sharing services (think Uber) this is now true of many other places, and large numbers of city dwellers are forgoing a vehicle entirely.

But are these trends the same in Auckland, Wellington or Christchurch?

Probably not, but monthly vehicle subscriptions may still have a place in NZ and quite a few reputable companies think so too. Recently, Turners announced they had purchased a stake in the Aussie company Carly and plan to launch in NZ later this year; Mercury Energy partnered with Snap Rentals in 2018 to launch Drive, a subscription model exclusively for electric vehicles;Finance company Simplify now offer subs on vehicles ranging from three to twelve months and Cityhop provide even more flexibility, allowing subs for as little as four weeks at a time.

And it’s not just second-hand cars either. In the US, vehicle manufacturers like Porsche, Audi, BMW, Cadillac, Nissan and Volvo are all offering their own version of monthly subscriptions. It’s coming people!

So how do monthly vehicle subscriptions typically work?

In most cases you pick a car, sign up for a given period (say 3 or 6 months), and get full access to it as if you owned it outright. Payment is taken weekly after the first month and includes insurance, registration, roadside assistance and routine maintenance. In some cases, you can switch the car you’ve chosen, either throughout the sub or at the end of each term.

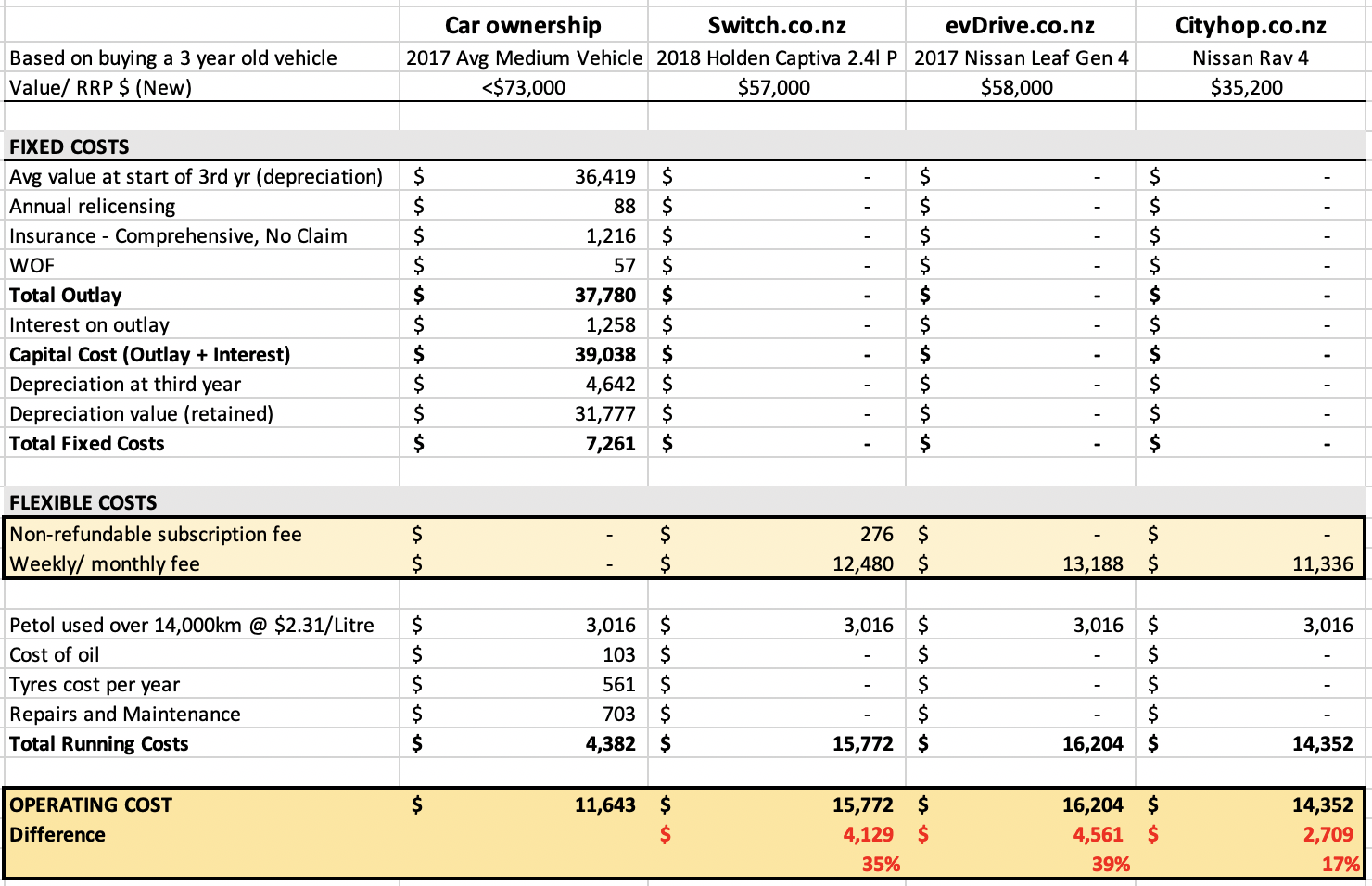

Do the financials stack up?

Obviously this depends on your usage, however it’s clear that you definitely pay a premium for the convenience.

Every year the AA breakdown the cost of owning a car for each of the main car categories (small/ compact/ medium, petrol/ diesel/ hybrid etc). This analysis allows for current fuel and oil prices, the latest prices for maintenance and tyres, but most importantly calculates the cost of depreciation (the devil when it comes to car ownership). It helps provide a comprehensive comparison against the cost of a monthly vehicle subscription.

We’ve focussed on the medium-sized, petrol car category, however, the results are reflective of each category. Over a 12-month period, taking a loan to buy a car worked out between 17% and 39% cheaper than an equivalent monthly subscription. This factored in finance, WOF, insurance, repairs and maintenance, the lot. Check out the table below to see the specifics. And once the car is fully paid off, you own it. It’s an asset, with some retained value that you can sell.

How is this different from leasing a car?

The main difference here is the term. Most leases are set up over a longer period of time, often around 3 years. They are also more common on new cars, where vehicles have higher initial values, and where a longer-term is required to depreciate over.

Is a vehicle subscription accessible to everyone?

Yes, as long as you are over 21 years old and have a full driver’s licence. Depending on the service, you’ll likely need to prove you are good for the money as well, which might mean bank statements, utility bills and/or credit scores.

Are there catches?

Unfortunately so. Some providers charge an upfront non-refundable subscription fee. Then there is a long list of fees and charges typical for finance companies including things like cancellation fees, transaction fees, mortgage fees, late fees, cleaning fees etc. Note, these are different for each provider.

If you’re a big driver you’ll want to know about the maximum km per month, which apply to some providers. Insurance excesses look pretty steep at around $1,000, and you’ll need a little money to get started, around 50% of the first month’s sub, with the difference being charged 15 days later.

In our opinion, this is one of those times it’s worth reading the terms and conditions thoroughly.

The reality is that this isn’t going to appeal to everyone. If you have the money or don’t mind taking a loan to buy a car, you’ll end up saving over the medium term by buying a car. The range of vehicles on offer is also pretty limited, and it is unlikely you’ll be able to find your dream car on subscription. Kiwi’s take pride in owning their first (and subsequent) cars and that makes it somewhat of an irrational purchase for many. We have one of the highest car ownership per capita in the world (0.8 per capita in 2018), and for a lot of people, their car is their biggest asset. These cultural changes will take time to imbed.

This doesn’t preclude the idea from taking off in the future. New providers appear to be popping up all over the place, and shortly there will be enough of them to create a competitive market that should drive down pricing and make the maths stack up for customers.

With car manufacturers trialling the model in the US it’s probable the appeal of new cars on monthly subscription could gather further interest in the idea. Especially if it’s a new Porsche.

Until then, I’ll keep saving up to buy my next car.